Insider filing report for Changes in Beneficial Ownership

- Schedule 13G & 13D forms are used to report a party's ownership of stock which exceeds 5% of a company's total stock issue.

- Schedule 13G is a shorter version of Schedule 13D with fewer reporting requirements.

- Peter Lynch

What is insider trading>>

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

SCHEDULE 13D

THE SECURITIES EXCHANGE ACT OF 1934

(Amendment No. 4)*

| Global Indemnity Group, LLC |

| (Name of Issuer) |

| Class A Common Stock |

| (Title of Class of Securities) |

| 37959R103 |

| (CUSIP Number) |

|

Kevin A. McGovern, Esq. c/o Harbert Fund Advisors, Inc. 2100 Third Avenue North Suite 600 Birmingham, AL 35203 Telephone Number 205-987-5500 |

|

(Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications) |

| August 12, 2021 |

| (Date of Event Which Requires Filing of this Statement) |

| If the filing person has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of ss.240.13d-1(e), 240.13d-1(f) or 240.13d-1(g), check the following box [_]. | |

| * The remainder of this cover page shall be filled out for a reporting person's initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing information which would alter disclosures provided in a prior cover page. | |

CUSIP No. |

37959R103 |

| 1. | NAME OF REPORTING PERSONS | |

| I.R.S. IDENTIFICATION NOS. OF ABOVE PERSONS (ENTITIES ONLY) | ||

| Harbert Fund Advisors, Inc. |

| 2. | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP | (a) | [_] |

| (b) | [_] |

| 3. | SEC USE ONLY | |

| 4. | SOURCE OF FUNDS | |

| AF |

| 5. | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDINGS IS REQUIRED PURSUANT TO ITEMS 2(d) OR 2(e) | [_] |

| 6. | CITIZENSHIP OR PLACE OF ORGANIZATION | |

| Alabama |

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON |

| 7. | SOLE VOTING POWER | |

| 0 |

| 8. | SHARED VOTING POWER | |

| 849,985 |

| 9. | SOLE DISPOSITIVE POWER | |

| 0 | ||

| 10. | SHARED DISPOSITIVE POWER | |

| 849,985 |

| 11. | AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH REPORTING PERSON | |

| 849,985 |

| 12. | CHECK BOX IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | [_] |

| 13. | PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) | |

| 8.1% |

| 14. | TYPE OF REPORTING PERSON | |

| IA, CO | ||

CUSIP No. |

37959R103 |

| 1. | NAME OF REPORTING PERSONS | |

| I.R.S. IDENTIFICATION NOS. OF ABOVE PERSONS (ENTITIES ONLY) | ||

| Harbert Management Corporation |

| 2. | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP | (a) | [_] |

| (b) | [_] |

| 3. | SEC USE ONLY | |

| 4. | SOURCE OF FUNDS | |

| AF |

| 5. | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDINGS IS REQUIRED PURSUANT TO ITEMS 2(d) OR 2(e) | [_] |

| 6. | CITIZENSHIP OR PLACE OF ORGANIZATION | |

| Alabama |

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON |

| 7. | SOLE VOTING POWER | |

| 0 |

| 8. | SHARED VOTING POWER | |

| 849,985 |

| 9. | SOLE DISPOSITIVE POWER | |

| 0 | ||

| 10. | SHARED DISPOSITIVE POWER | |

| 849,985 |

| 11. | AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH REPORTING PERSON | |

| 849,985 |

| 12. | CHECK BOX IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | [_] |

| 13. | PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) | |

| 8.1% |

| 14. | TYPE OF REPORTING PERSON | |

| CO | ||

CUSIP No. |

37959R103 |

| 1. | NAME OF REPORTING PERSONS | |

| I.R.S. IDENTIFICATION NOS. OF ABOVE PERSONS (ENTITIES ONLY) | ||

| Jack Bryant |

| 2. | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP | (a) | [_] |

| (b) | [_] |

| 3. | SEC USE ONLY | |

| 4. | SOURCE OF FUNDS | |

| AF |

| 5. | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDINGS IS REQUIRED PURSUANT TO ITEMS 2(d) OR 2(e) | [_] |

| 6. | CITIZENSHIP OR PLACE OF ORGANIZATION | |

| United States of America |

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON |

| 7. | SOLE VOTING POWER | |

| 0 |

| 8. | SHARED VOTING POWER | |

| 849,985 |

| 9. | SOLE DISPOSITIVE POWER | |

| 0 | ||

| 10. | SHARED DISPOSITIVE POWER | |

| 849,985 |

| 11. | AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH REPORTING PERSON | |

| 849,985 |

| 12. | CHECK BOX IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | [_] |

| 13. | PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) | |

| 8.1% |

| 14. | TYPE OF REPORTING PERSON | |

| IN | ||

CUSIP No. |

37959R103 |

| 1. | NAME OF REPORTING PERSONS | |

| I.R.S. IDENTIFICATION NOS. OF ABOVE PERSONS (ENTITIES ONLY) | ||

| Kenan Lucas |

| 2. | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP | (a) | [_] |

| (b) | [_] |

| 3. | SEC USE ONLY | |

| 4. | SOURCE OF FUNDS | |

| AF |

| 5. | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDINGS IS REQUIRED PURSUANT TO ITEMS 2(d) OR 2(e) | [_] |

| 6. | CITIZENSHIP OR PLACE OF ORGANIZATION | |

| United States of America |

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON |

| 7. | SOLE VOTING POWER | |

| 0 |

| 8. | SHARED VOTING POWER | |

| 849,985 |

| 9. | SOLE DISPOSITIVE POWER | |

| 0 | ||

| 10. | SHARED DISPOSITIVE POWER | |

| 849,985 |

| 11. | AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH REPORTING PERSON | |

| 849,985 |

| 12. | CHECK BOX IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | [_] |

| 13. | PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) | |

| 8.1% |

| 14. | TYPE OF REPORTING PERSON | |

| IN | ||

CUSIP No. |

37959R103 |

| 1. | NAME OF REPORTING PERSONS | |

| I.R.S. IDENTIFICATION NOS. OF ABOVE PERSONS (ENTITIES ONLY) | ||

| Raymond Harbert |

| 2. | CHECK THE APPROPRIATE BOX IF A MEMBER OF A GROUP | (a) | [_] |

| (b) | [_] |

| 3. | SEC USE ONLY | |

| 4. | SOURCE OF FUNDS | |

| AF |

| 5. | CHECK BOX IF DISCLOSURE OF LEGAL PROCEEDINGS IS REQUIRED PURSUANT TO ITEMS 2(d) OR 2(e) | [_] |

| 6. | CITIZENSHIP OR PLACE OF ORGANIZATION | |

| United States of America |

| NUMBER OF SHARES BENEFICIALLY OWNED BY EACH REPORTING PERSON |

| 7. | SOLE VOTING POWER | |

| 0 |

| 8. | SHARED VOTING POWER | |

| 849,985 |

| 9. | SOLE DISPOSITIVE POWER | |

| 0 | ||

| 10. | SHARED DISPOSITIVE POWER | |

| 849,985 |

| 11. | AGGREGATE AMOUNT BENEFICIALLY OWNED BY EACH REPORTING PERSON | |

| 849,985 |

| 12. | CHECK BOX IF THE AGGREGATE AMOUNT IN ROW (11) EXCLUDES CERTAIN SHARES | [_] |

| 13. | PERCENT OF CLASS REPRESENTED BY AMOUNT IN ROW (11) | |

| 8.1% |

| 14. | TYPE OF REPORTING PERSON | |

| IN | ||

| CUSIP No. | 37959R103 | ||

| Item 1. | Security and Issuer. |

| The name of the issuer is Global Indemnity Group, LLC, a Delaware corporation (the "Issuer"). The address of the Issuer's principal executive offices is 3 Bala Plaza East, Suite 300, Bala Cynwyd, PA 19004, United States of America. This Schedule 13D relates to the Issuer's Class A Common Stock, (the "Shares"). | ||

| Item 2. | Identity and Background. |

| (a) |

This Schedule 13D is being filed jointly by

(i) Harbert Fund Advisors, Inc., an Alabama corporation (“HFA”),

(ii) Harbert Management Corporation, an Alabama corporation (“HMC”),

(iii) Jack Bryant, a United States citizen,

(iv) Kenan Lucas, a United States citizen, and

(v) Raymond Harbert, a United States citizen.

Each of HFA, HMC, Mr. Bryant, Mr. Lucas and Mr. Harbert are referred to as a “Reporting Person” and collectively as the “Reporting Persons.” Each of the Reporting Persons is party to that certain Joint Filing Agreement attached hereto as Exhibit A. Accordingly, the Reporting Persons are hereby filing a joint Schedule 13D. This statement relates to Shares held for the account of certain client accounts (the “Clients”) for which HFA acts as investment manager. HFA is an investment adviser registered with the United States Securities and Exchange Commission. HMC Is the parent of HFA. Mr. Lucas is the portfolio manager for the Clients. Mr. Bryant is an Executive Vice President and Senior Managing Director of HMC. Mr. Harbert is the Chairman and Chief Executive Officer of HMC and HFA.

Set forth on Exhibit B attached hereto is the name and present principal occupation or employment, principal business address and citizenship of the executive officers and directors of HFA and HMC. To the best of the Reporting Persons’ knowledge, except as otherwise set forth herein, none of the persons listed on Exhibit B beneficially owns any securities of the Issuer or is a party to any contract, agreement or understanding required to be disclosed herein. |

||

| (b) | The principal business address for each of the Reporting Persons is 2100 Third Avenue North, Suite 600, Birmingham, Alabama 35203. | ||

| (c) | The principal business of HMC and its wholly-owned subsidiary HFA is serving as an alternative asset management firm to various private funds. The principal business of Mr. Lucas is serving as the Managing Director and Portfolio Manager of the general partner of Harbert Discovery Fund, LP and as the portfolio manager for the Clients. The principal business of Mr. Bryant is serving as an Executive Vice President and Senior Managing Director of HMC. The principal business of Mr. Harbert is serving as the Chairman and Chief Executive Officer of HMC and HFA. | ||

| (d) | No Reporting Person or any person listed on Exhibit B has, during the last five years, been convicted in a criminal proceeding (excluding traffic violations or similar misdemeanors). | ||

| (e) | No Reporting Person or any person listed on Exhibit B has, during the last five years, been a party to a civil proceeding of a judicial or administrative body of competent jurisdiction and as a result of such proceeding was or is subject to a judgment, decree or final order enjoining future violations of, or prohibiting or mandating activities subject to, Federal or state securities laws or finding any violation with respect to such laws. | ||

| (f) | Mr. Lucas, Mr. Bryant and Mr. Harbert are each a citizen of the United States of America. HFA and HMC are incorporated under the laws of the State of Alabama. The citizenship of the persons listed on Exhibit B is set forth therein. | ||

| Item 3. | Source and Amount of Funds or Other Consideration. | |

| The funds for the purchase of the Shares came from the working capital of the Clients, ov er which HFA, HMC, Jack Bryant, Kenan Lucas and Raymond Harbert, through their roles described above in Item 2(c), exercise investment discretion. No borrowed funds were used to purchase the Shares, other than borrowed funds used for working capital purposes in the ordinary course of business. The total costs of the Shares directly owned by the Clients is approximately $21,066,148. | ||

| Item 4. | Purpose of Transaction. | |

| The Reporting Persons sent the letter attached in Exhibit D to the Chairman of the Issuer’s Board of Directors. Other than the foregoing, there have been no changes to the Schedule 13D Amendment No. 3 filed on May 19, 2021. | ||

| Item 5. | Interest in Securities of the Issuer. | ||

| (a) - (e) |

As of the date hereof, (i) HFA, HMC, Jack Bryant, Kenan Lucas and Raymond Harbert may be deemed to be the beneficial owners of 849,985 Shares, constituting 8.1% of the Shares, based upon *10,515,177 Shares outstanding.

HFA has the sole power to vote or direct the vote of 0 Shares; has the shared power to vote or direct the vote of 849,985 Shares; has the sole power to dispose or direct the disposition of 0 Shares; and has the shared power to dispose or direct the disposition of 849,985 Shares.

HMC has the sole power to vote or direct the vote of 0 Shares; has the shared power to vote or direct the vote of 849,985 Shares; has the sole power to dispose or direct the disposition of 0 Shares; and has the shared power to dispose or direct the disposition of 849,985 Shares.

Jack Bryant has the sole power to vote or direct the vote of 0 Shares; has the shared power to vote or direct the vote of 849,985 Shares; has the sole power to dispose or direct the disposition of 0 Shares; and has the shared power to dispose or direct the disposition of 849,985 Shares.

Kenan Lucas has the sole power to vote or direct the vote of 0 Shares; has the shared power to vote or direct the vote of 849,985 Shares; has the sole power to dispose or direct the disposition of 0 Shares; and has the shared power to dispose or direct the disposition of 849,985 Shares.

Raymond Harbert has the sole power to vote or direct the vote of 0 Shares; has the shared power to vote or direct the vote of 849,985 Shares; has the sole power to dispose or direct the disposition of 0 Shares; and has the shared power to dispose or direct the disposition of 849,985 Shares.

The transactions by the Reporting Persons in the securities of the Issuer since the initial Schedule 13D are set forth in Exhibit C. All such transactions were carried out in open market transactions.

*This outstanding Shares figure reflects the number of outstanding Class A Common Shares at July 28, 2021. |

||

| Item 6. | Contracts, Arrangements, Understandings or Relationships with Respect to Securities of the Issuer. | |

| The holdings listed above are held by the Clients. | ||

| Item 7. | Material to be Filed as Exhibits. |

|

Exhibit A: Joint Filing Agreement Exhibit B: Officers and Directors of HFA and HMC Exhibit C: Schedule of Transactions in Shares Exhibit D: Letter to GBLI Chairman Fox | ||

SIGNATURE

After reasonable inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| August 12, 2021 | |||

| (Date) |

| Harbert Fund Advisors, Inc.* | |||

| By: |

/s/ John McCullough |

||

| Executive Vice President and General Counsel |

|||

| Harbert Management Corporation* | |||

| By: |

/s/ John McCullough |

||

| Executive Vice President and General Counsel |

|||

|

/s/ Jack Bryant* |

|||

| Jack Bryant | |||

|

/s/ Kenan Lucas* |

|||

| Kenan Lucas | |||

|

/s/ Raymond Harbert* |

|||

| Raymond Harbert | |||

* This reporting person disclaims beneficial ownership of these reported securities except to the extent of its pecuniary interest therein, and this report shall not be deemed an admission that any such person is the beneficial owner of these securities for purposes of Section 16 of the U.S. Securities Exchange Act of 1934, as amended, or for any other purpose.

Attention: Intentional misstatements or omissions of fact constitute Federal criminal violations (see 18 U.S.C. 1001).

Exhibit A

AGREEMENT

The undersigned agree that this amendment number four to the Schedule 13D relating to the Class A Common Stock of Global Indemnity Group, LLC. shall be filed on behalf of the undersigned.

| August 12, 2021 | |||

| (Date) |

| Harbert Fund Advisors, Inc. | |||

| By: |

/s/ John McCullough |

||

| Executive Vice President and General Counsel |

|||

| Harbert Management Corporation | |||

| By: |

/s/ John McCullough |

||

| Executive Vice President and General Counsel |

|||

|

/s/ Jack Bryant |

|||

| Jack Bryant | |||

|

/s/ Kenan Lucas |

|||

| Kenan Lucas | |||

|

/s/ Raymond Harbert |

|||

| Raymond Harbert | |||

Exhibit B

Titled Officers and Directors of Harbert Fund Advisors, Inc. and Harbert Management Corporation

| Name and Position | Principal Occupation | Principal Business Address | Citizenship | |||

|

Raymond J. Harbert Chief Executive Officer and Chairman of HFA and HMC |

Serving as Chairman and CEO of HMC |

2100 Third Avenue North, Suite 600; Birmingham, AL 35203 |

USA | |||

|

John F. Bryant Executive Vice President and Director of HMC |

Serving as Executive Vice President and a Director of HMC |

2100 Third Avenue North, Suite 600; Birmingham, AL 35203 |

USA | |||

|

Charles D. Miller Executive Vice President of HFA and HMC |

Serving as EVP of HMC |

2100 Third Avenue North, Suite 600; Birmingham, AL 35203 |

USA | |||

|

Raymond J, Harbert, Jr. Executive Vice President & Chief Financial Officer of HFA and HMC & Director of HMC |

Serving as EVP, CFO and a director of HMC |

2100 Third Avenue North, Suite 600; Birmingham, AL 35203 |

USA | |||

|

John W. McCullough Executive Vice President, General Counsel & Director of HFA and HMC |

Serving as EVP, GC and a director of HMC |

2100 Third Avenue North, Suite 600; Birmingham, AL 35203 |

USA | |||

|

J. Travis Pritchett President & Chief Operating Officer of HFA and HMC & Director of HMC |

Serving as President, COO and a director of HMC |

2100 Third Avenue North, Suite 600; Birmingham, AL 35203 |

USA | |||

|

Michael C. Bauder Chief Compliance Officer of HFA and HMC & Director of HFA |

Serving as CCO of HFA and HMC and a Director of HFA | 2100 Third Avenue North, Suite 600; Birmingham, AL 35203 | USA |

Exhibit C

Schedule of Transactions in Shares

The Reporting Persons have not transacted in shares of the Issuer in the past 60 days.

Exhibit D

Letter to GBLI Chairman Fox

Birmingham, AL

August 12, 2021

Mr. Saul Fox, Chairman of the Board of Directors

Global Indemnity Group, LLC

Three Bala Plaza East

Suite 300

Bala Cynwyd, PA 19004

By Federal Express and email

Chairman Fox,

Global Indemnity Group, LLC’s (“GBLI” or the “Company”) recent results show that the ~$250 million of surplus capital is dragging down the overall returns of the business, and the core returns from the insurance operations have significantly underperformed peers during the best environment for the industry in years. At a time when GBLI should be able to take advantage of its excess capital to nimbly and aggressively drive profitable growth, GBLI has failed to deliver. Consequently, GBLI’s shares continue to languish, with a worst-in-class valuation multiple. We believe these results further demonstrate that the best use of the excess capital freed up by the redomestication scheme is to immediately return that capital to shareholders via a special dividend and/or a share repurchase.

In your May 24 response to the letter we sent you on May 19, you communicated that “we may not share the same strategic vision for the Company.” Yet to date you have neither engaged in a meaningful dialogue with us nor communicated your strategic vision for the Company to all shareholders. We expect you will remedy this deficiency at the September 13 investor day by either disclosing your plans to immediately return the excess capital or describing (in detail with specifics) how that capital can be put to use to deliver a better risk adjusted return for shareholders, in spite of the significant evidence to the contrary.

We urge you to detail how the business will be managed for the best interest of all shareholders, as is required by your fiduciary duty. The long history of questionable and expensive strategic actions, coupled with the excessive fee payments to Fox Paine, appear to indicate a strong preference for collecting fees rather than managing the business in the best interest of all shareholders. With the change in management incentive compensation away from restricted stock, it appears you are moving further away from aligning the incentives of insiders with the independent shareholders. This is unacceptable. You have chosen to run GBLI as a public company with independent shareholders, but if you cannot or will not run the Company with their interests in mind, then you should take GBLI private.

We received significant shareholder support following our prior letter. Shareholders expect much greater transparency into the business, in addition to a more shareholder friendly capital allocation strategy. If the Company has any interest in addressing the persistent underperformance and worst-in-class valuation multiple, GBLI must be much more transparent in how the business is being managed. In fact, while you have publicly stated that there will be an Investor Day on September 13, you still have not disclosed the exact time or location of the event. The exact time and location should be immediately disclosed so that shareholders, the owners of the business, are afforded the opportunity to attend that event and ask questions of management and the GBLI Board of Directors (the “Board”).

Following are a list of questions that we expect you, management, and the Board to address at the upcoming Investor Day. We encourage all shareholders to voice their concerns as well, and reiterate that you and the Board have a fiduciary duty to all shareholders, regardless of the Company’s control provisions.

Why is GBLI underperforming to such a significant degree during the best environment for the industry in years? If the Company had the capability to utilize the excess capital in order to support profitable organic growth, we would have expected it to show in GBLI’s fundamental results. Given the magnitude of excess capital relative to the current operations and relative size of GBLI, the Company should be able to nimbly and aggressively take advantage of the current pricing environment. However, GBLI has significantly underperformed peers in terms of underwriting and growth. Industry peers have generated banner profitability and growth, with many significantly large companies exceeding 20% net written premium (“NWP”) growth in the second quarter. Conversely, after three straight quarters of underwriting losses, GBLI’s Q2 was only slightly profitable with single-digit NWP growth.

What is the best use of the excess ~$250 million, if not to return the capital to shareholders? Recent results do not support the case for organic growth. Based on GBLI’s history and the years of underperformance following the 2015 acquisition of American Reliable, we do not believe an acquisition is in the best interest of shareholders. The Company paid $100 million for the American Reliable acquisition, not including $6.5 million of fees to Fox Paine or $5.1 million of additional professional fees to third parties. In the Company’s 2020 investor presentation, you highlighted the $7.9 million profit generated in 2019 from the Specialty Property segment as evidence that GBLI had finally turned around American Reliable. This was after the segment significantly underperformed expectations from the outset, including losing $47.9 million in 2018. Then in 2020, Specialty Property again underperformed, losing $16.9 million. Clearly, the segment had not been turned around, and the acquisition has been a drastic misallocation of resources. With the losses incurred to date and the fees paid in conjunction with the American Reliable acquisition, it would take decades of consistent, above average results for this transaction to deliver an acceptable outcome for shareholders. Another acquisition is not in shareholders’ best interest.

______________________

1 Data per Bloomberg and company filings. Peers include: AMSF, EIG, CB, RLI, SIGI, WRB, MKL, ORI, HCI, THG, AFG, TRV, HRTG, KMPR, Y, DGICA, JRVR, ARGO, and AIZ.

2 Data per Bloomberg and company filings. Peers include: AMSF, EIG, CB, SIGI, WRB, MKL, ORI, HCI, THG, AFG, TRV, KMPR, Y, DGICA, and JRVR.

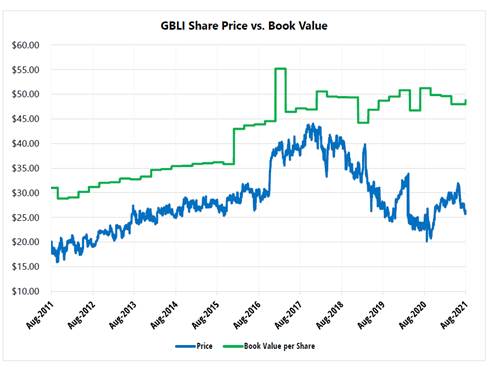

How will you address the persistent discount between the stock price and the Company’s book value? GBLI has not traded at or above book value for the last ten years. On average, the stock has traded at 0.7x book value. 3

We believe the main reasons for this are the excess capital, concerns regarding the fees paid to Fox Paine, lack of transparency, and the long history of anemic book value growth. In fact, GBLI’s book value per share has declined from a high of $55.19 at the end of 2016 to $48.79 today, in part as a result of the Company’s apparent focus on transactions that generate fees for Fox Paine at the cost of profitably growing the business. The negative impact of these transactions and the excess capital also shows in GBLI’s five year average return on equity of 2.0%, compared to a peer average of 8.1%.4

Given the underperformance and the apparent preference for generating fees for yourself at the expense of growing book value for all shareholders, it is no wonder that the share price has underperformed the KBW Property & Casualty ETF by over 60% over the last five years.5

______________________

3 Data per Bloomberg.

4 Data per Bloomberg and company filings. Peers include: AMSF, EIG, CB, RLI, SIGI, WRB, MKL, ORI, HCI, THG, AFG, TRV, HRTG, KMPR, Y, DGICA, JRVR, ARGO, and AIZ.

5 Data per Bloomberg. GBLI and KBW Property& Casualty ETF normalized to 100 from August 4, 2016.

We believe there is a significant opportunity to address this discount and underperformance by returning the excess capital to shareholders, delivering on the potential afforded the Company by the favorable industry backdrop, and ceasing all transactions/reorganizations that only serve to generate fees for yourself.

Why did you choose not to disclose Fox Paine’s fee associated with the redomestication when you issued the proxy statement to seek shareholder approval for the transaction? We question whether shareholders would have voted the same way had they known the extent to which you would benefit from the redomestication, particularly without more insight into the purpose of the transaction. It has been nearly a year since the redomestication and, other than the extremely vague for “general corporate purposes” description, you have still not disclosed the plans for the $250 million of excess, and immediately disbursable, capital which was moved up to the parent company as part of the redomestication.

Was the goal of converting to an LLC from a Corporation to force the Index funds to sell so you could buy shares at a discount? LLCs cannot be members of the Russell 2000 Index. As a result, Russell 2000 ETFs that held GBLI shares were forced to sell immediately after the conversion was approved. This resulted in millions of shares sold in the days following the shareholder meeting, when normally only 10,000 to 15,000 shares would trade in a day. The stock traded at an intraday low of $17.01 on August 27, 2020, down 32% from its close the day before. It appears you were prepared for this forced selling as you purchased 891,166 shares, or $20.7 million of stock, between August 28, 2020 and September 3, 2020. Furthermore, GBLI shareholders now receive K-1s, which significantly limits the number of investors willing to purchase shares. Unless you plan to return the excess capital to shareholders, we do not see any rationale for converting from a corporation to an LLC. Based on your actions and lack of strategic communications to date, we can only conclude that the intention of converting to an LLC was for you to take advantage of the forced selling by Index Funds.

Do the independent directors consider the expected return on the transactions advised by Fox Paine, including the fees they pay you? Since 2015, GBLI has paid Fox Paine $42 million of transaction-related fees and $13 million in management fees. In 2015, GBLI paid Fox Paine $6.5 million for advising on the American Reliable acquisition, which we noted above has not generated value for shareholders other than yourself. This was in addition to $5.1 million of additional professional fees for that transaction. Even ignoring the horrendous return the transaction has generated to date, a total fee burden that exceeds 10% of the transaction value appears wildly excessive and certainly is not customary.

In 2017, the Board approved an advisory payment of $11.0 million to Fox Paine for advising on an $83.0 million share repurchase. A share repurchase at a discount to book value is clearly accretive to shareholder value, and we would be supportive of additional share repurchases with the current excess capital. However, we cannot begin to fathom the rationale for a fee that is equivalent to 13% of the value of the shares repurchased.

As we have noted repeatedly, the 2020 redomestication transaction would create shareholder value if you return the excess capital to shareholders. Barring a return of capital, the reduction in expenses is expected to be offset by higher taxes. As a result, the only beneficiaries thus far are yourself and your entity, Fox Paine, not all shareholders. Similarly, it is unclear whether the 2018 reorganization, in which GBLI paid a $12.5 million transaction fee to Fox Paine, created any shareholder value, particularly since much of that appears to have been unwound as part of the 2020 redomestication.

As shareholders, we ask the independent directors of the Company to carefully and thoughtfully contemplate how the Company’s resources are allocated. The table below highlights the combined $55 million of fees paid to Fox Paine since 2015.

| Fox Paine Fees (millions) | |||||||||

| Year | Management Fee | Transaction Fee | Event | ||||||

| 2015 | $ | 1.9 | $ | 6.5 | American Reliable Acquisition | ||||

| 2017 | $ | 2.2 | $ | 11.0 | Share redemption | ||||

| 2018 | $ | 2.1 | $ | 2.0 | Sale of Illiquid Investment | ||||

| 2018 | $ | 12.5 | Corporate Reorganization | ||||||

| 2019 | $ | 2.1 | |||||||

| 2020 | $ | 2.6 | $ | 10.0 | Redomestication | ||||

| Total | $ | 13.0 | $ | 42.0 | |||||

| 6 | |||||||||

Under what circumstances would you consider selling GBLI to a strategic acquirer? We are aware that you have historically considered selling GBLI, that there were interested buyers in the past, and understand there would be interested buyers today. Shareholders would have been better off receiving a premium to book value for their GBLI shares at any point over the last ten years and reinvesting the proceeds in industry peers. The current M&A and industry pricing environment provide a compelling backdrop for a sale. Moreover, given the recent fundamental performance, a larger strategic buyer would likely be capable of generating significantly better results than the Company has delivered over the last five years.

Are you considering taking the company private yourself? CEO David Charlton’s Book Value Appreciation Rights accelerate in a change of control transaction. However, his employment agreement excludes an acquisition by a Fox Paine-related entity from the change of control definition. Is the reason you have not returned the excess capital to shareholders that you plan to utilize it to help fund a take private transaction at a favorable price? What assurances do shareholders have that the Board will truly represent the interests of all shareholders and ensure a fair price in the event of a take-private by Fox Paine?

We will attend the Investor Day Conference on September 13, and we look forward to asking additional questions, meeting the new management team, and discussing their plans to deliver on the aggressive targets outlined in their employment agreements. However, there is no need to wait until September, over a year after the redomestication, to either return the excess capital that was freed up as part of that transaction or to disclose an alternate use that offers a better risk-adjusted return for all shareholders.

______________________

6 Data per company filings.

I continue to prefer a path where we can have private conversations that are not in the public sphere. I think it would be more productive if I could speak directly with you and the Board.

Please do not squander this opportunity to generate immediate and real value. Shareholders deserve better.

Sincerely,

Harbert Discovery Fund, LP

Kenan Lucas, Managing Director and Portfolio Manager of Harbert Discovery Fund GP, LLC